All in on AI? 3 ways to reduce concentration risk

Hugh Lam

6 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Betashares Senior Investment Strategist Cameron Gleeson recently sat down with Cameron Mitchell, ANZ’s Head of Geopolitical Risk, to explore how geopolitical shifts are reshaping economics and business, and the impact on market dynamics.

Below we look at five key takeaways from the webinar and potential investment opportunities under a second Trump administration and a new global order.

To view a recording of the webinar, click here.

1. The convergence of geopolitics and business [3:00]

As major power competition increases, so too has the convergence of geopolitics and business.

Traditionally, geopolitical concerns have been top-down where governments make decisions that then impact businesses. For example, the US government recently implemented technology export controls on American-made AI chips to protect national security interests.

What we are seeing now are bottom-up impacts as well.

As Cameron Mitchell mentioned at the 4:30 mark of the webinar – following the aftermath of the Russian invasion of Ukraine, we saw upwards of 1,000 Western companies either freezing their operations in Russia or leaving the market. That was not driven by sanctions or policy requirements from governments.

Click on the thumbnail below to visit the webinar recording.

2. Systematic impact events [5:00]

The rise of systematic impact events – those that create significant shocks over a long period of time – will have second and third order effects for the world that can be difficult at first to measure.

A few of these events to be wary of include:

- The rise of China leading to global realignments in trade and diplomacy, increased de-dollarisation efforts and increased industrial policy. China’s share of global production is now higher than the next nine global manufacturing economies combined.

- Partisan US foreign policy leading to lacklustre commitments to multilateral agreements (e.g., Iran nuclear deal, climate agreements), short-termism and limited capacity to address global issues.

- Russia’s invasion of Ukraine leading to global financial dislocation, energy and food insecurity.

3. 2020s will be critical to determining the outcome of key global relationships and challenges [11:15]

Cameron Mitchell highlights the ‘UNTIDI’ decade of the 2020s as a framework to determine the outcome of key global relationships and challenges.

U – Uneven energy transition

- The energy transition is likely to be bumpy, with some fossil fuel and renewable energy dominant countries using their geopolitical weight to their advantage.

N – New trading patterns

- New trading patterns are emerging with the US, its allies and its partners going through an onshoring phenomenon.

T – Trusted technologies

- There is a deepening technology divide between the US and China, with enterprises and governments seeking who to partner with.

I – Industrial policy

- Efforts to rectify shortcomings in sovereign production capacity across US, European and Asian developed markets have resulted in increasing levels of industrial policy – particularly in the technology, defence and energy sectors.

D – Defence

- There will be big boosts to global demand for defence as geopolitical risks rise.

I – Ideology

- We are seeing a more ideological foreign policy streak from countries, particularly since the Russian invasion of Ukraine, playing out across many frontier and emerging markets.

4. S&P 500 Equal Weight, India and the UK equity markets may benefit under a second Trump administration [27:35]

Some of Trump’s tariff and immigration policies have largely been viewed as a headwind for markets, however there may be potential beneficiaries in select exposures according to Cameron Gleeson, Senior Investment Strategist – Betashares.

With an ‘America First’ populist agenda, there may be a broadening out of equity market performance in sectors beyond Information Technology. This may favour an equal weighted exposure such as the QUS S&P 500 Equal Weight ETF , which aims to track the S&P 500 Equal Weight Index (before fees and expenses). This index is currently ~20% cheaper than a market cap weighted S&P 500 index on a forward price to earnings basis, while also forecast to return 13% growth in earnings over the next year1.

Countries like India and the UK may be net beneficiaries from increased tariffs and protectionism, given a large proportion of their exports are services-based. Trump’s tariffs are likely to impact manufactured goods and autos from China and Europe.

Source: UNCTAD, Haver Analytics, Goldman Sachs Research, June 2024. All values in U.S. dollars.

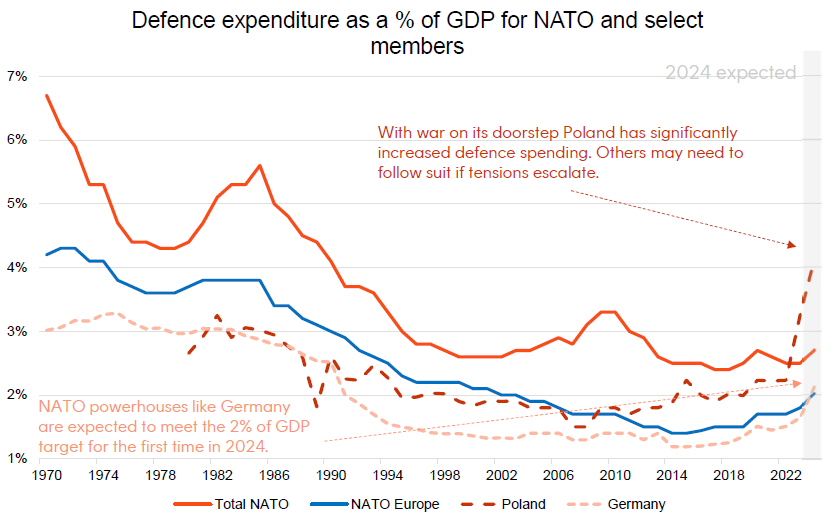

5. Commodities and defence security spending [38:30]

Cameron Gleeson also highlights that commodity exposures such as gold may provide an effective hedge within an investor’s portfolio during periods of escalating geopolitical tensions, as gold is often considered a ‘safe haven’ asset (i.e. an investment that may retain its value during periods of market turbulence).

Uranium is another commodity likely to benefit from a focus on greater energy security, as it’s a reliable, low-cost form of energy. While oil appears relatively well supplied in the West, uranium may form an interesting part of the mix if countries are looking to decarbonise and lower emissions.

And finally, given the geopolitical outlook, defence spending may increase as countries seek to strengthen their national security. We have already seen an uplift in European defence spending and the US may be incentivised to sign multi-billion-dollar defence deals with other nations to reduce its current account deficit.

Source: NATO. 1970 to 2024. 2024 numbers are NATO estimates.

You can watch the full webinar on replay here.

Potential investment opportunities if you want to take a position

-

QUS

S&P 500 Equal Weight ETF

- Domestically focused US companies have more to gain and less to lose from a possible trade war and protectionism. This could favour the S&P 500 Equal Weight Index (which QUS seeks to track, before fees and expenses) relative to the market cap weighted S&P 500 Index that is currently dominated by large global tech companies.

-

URNM

Global Uranium ETF

- Increased focus on energy security may favour reliable, low-cost forms of energy like uranium.

-

QAU

Gold Bullion Currency Hedged ETF

- Gold provides a natural geopolitical hedge to an investor’s portfolio and a rising US fiscal deficit may provide a structural tailwind for the yellow metal.

-

ARMR

Global Defence ETF

- Global defence contractors may receive a boost as European NATO countries increase their defence spending under a second Trump administration.

There are risks associated with an investment in the Funds including market risk, security specific risk, industry sector risk, index tracking risk, currency risk, concentration risk and for QAU, gold price risk. Investment value can go up and down. An investment in the Funds should only be considered as part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Funds, please see the relevant Product Disclosure Statement and Target Market Determination, both available on the Betashares website (www.betashares.com.au).

Source:

1. Bloomberg consensus estimates. As at November 2024. Actual results may differ materially from forecasts. ↑

Explore

Markets

1 comment on this

Are you able to elaborate on “deepening technology divide between the US and China”?