Rates relief

David Bassanese

5 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Global markets

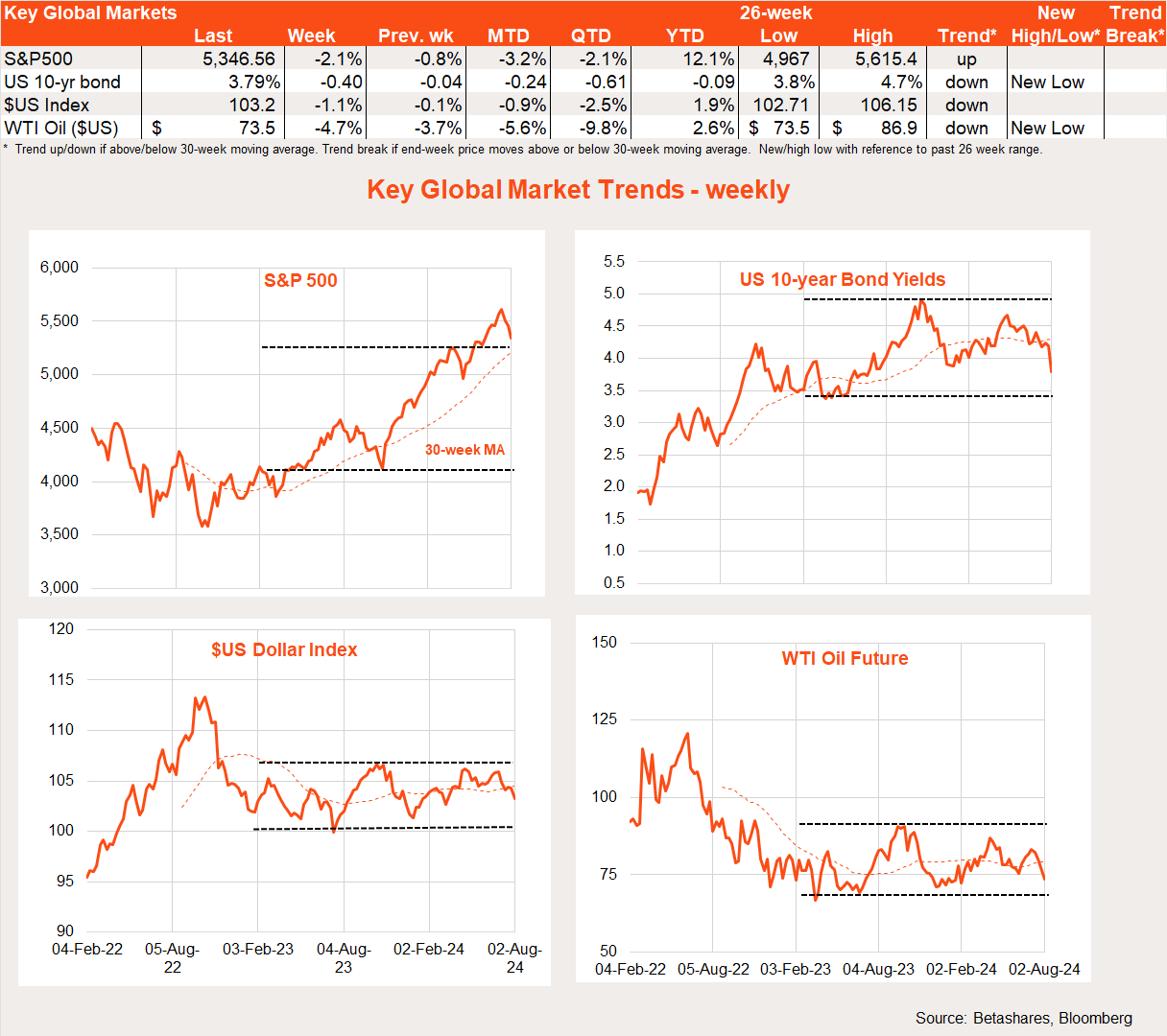

Weak US economic data and further disappointing earnings reports led to a further pullback in global equities last week, yet a strong rally in bonds. For the first time in a long time, bad news is bad news again.

Last week started somewhat promisingly, with the US Federal Reserve signalling a rate cut next month was “on the table” due to declining inflation. Yet the champagne was set aside by week’s end due to a weaker-than-expected US manufacturing report and, most importantly, the weaker-than-expected payrolls report.

The US ISM manufacturing index dipped to 46.8 in July (market 48.8), with forward orders and employment indices all weak. This is still above typical recessionary levels (for the overall economy) but does suggest high interest rates and a firm $US are finally starting to bite.

Weakness was also evident in the July payrolls report, with a soft 117k gain in employment and a lift in the unemployment rate from 4.1% to 4.3%. Average hourly earnings were a touch softer than expected, up 0.3% (market 0.2%).

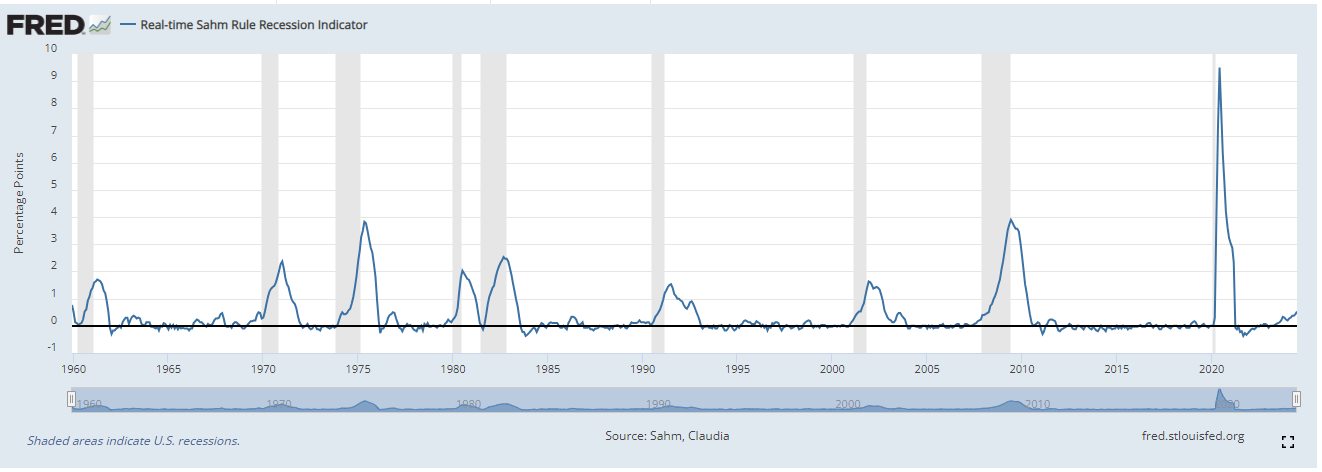

Note there is increasing chatter about the ‘Sahm rule’ which is an historical observation that every time the 3-month moving average of the US unemployment rate has lifted by 0.5% above its previous 12-month low, it has coincided with the beginning of a US recession – and a subsequent much larger rise in unemployment. That rule was triggered on Friday, and along with the long inverted US yield curve and earlier inflation surge is another historical recession indicator which will ultimately again be either vindicated or relegated to the dustbin of history.

My take? I can’t see a reason for a sudden US lurch into recession. As former RBA Governor Ian Macfarlane once observed, recessions usually arise from imbalances or shocks – and the US is not really suffering from either at present, with corporate and household balance sheets still in reasonable shape and inflation almost back to the Fed’s target level.

Rather, what we may be seeing is an easing back or ‘re-normalising’ in conditions after the post-COVID pressure cooker environment of extreme labour shortages and stimulus-driven demand. Of course, this negative dynamic could build momentum – inadvertently tipping the economy into at least a brief recession – a risk which the Fed is likely monitoring closely. The market is now almost fully pricing a 0.5% rate cut at the September policy meeting – which is not out of the question if economic data continue to weaken.

Adding to the equity market woes, earnings reports from key tech darlings – this time Amazon and Microsoft – continued to disappoint investors, adding to what has been a less than impressive earnings season so far.

In non-US news last week, the Bank of Japan bit the bullet and lifted interest rates further (also cutting back on bond purchases), with the resulting Yen strength continuing the unwinding of the outperforming bias of Japanese equities over the past year. The Bank of England cut rates (though the vote was surprisingly close) in light of its weak economy and return of inflation back to target.

Global week ahead

In light of new concerns over the health of the US economy, activity reports will now take on greater market importance – potentially even more than inflation reports.

In this regard, Tuesday’s US ISM non-manufacturing report will be keenly observed, with a lift to 51.4 from 48.8 expected – which could reassure investors of ongoing resilience in the services sector, despite weakness in manufacturing. Also of note will be Thursday’s weekly jobless claims report – which have also been rising of late though still at relatively low levels.

Market trends

As evident in the chart set below, the sell-off in equities over recent weeks has been harder for the growth/technology/quality areas than value. As noted above, Japan’s earlier outperformance continues to unwind.

Australian market

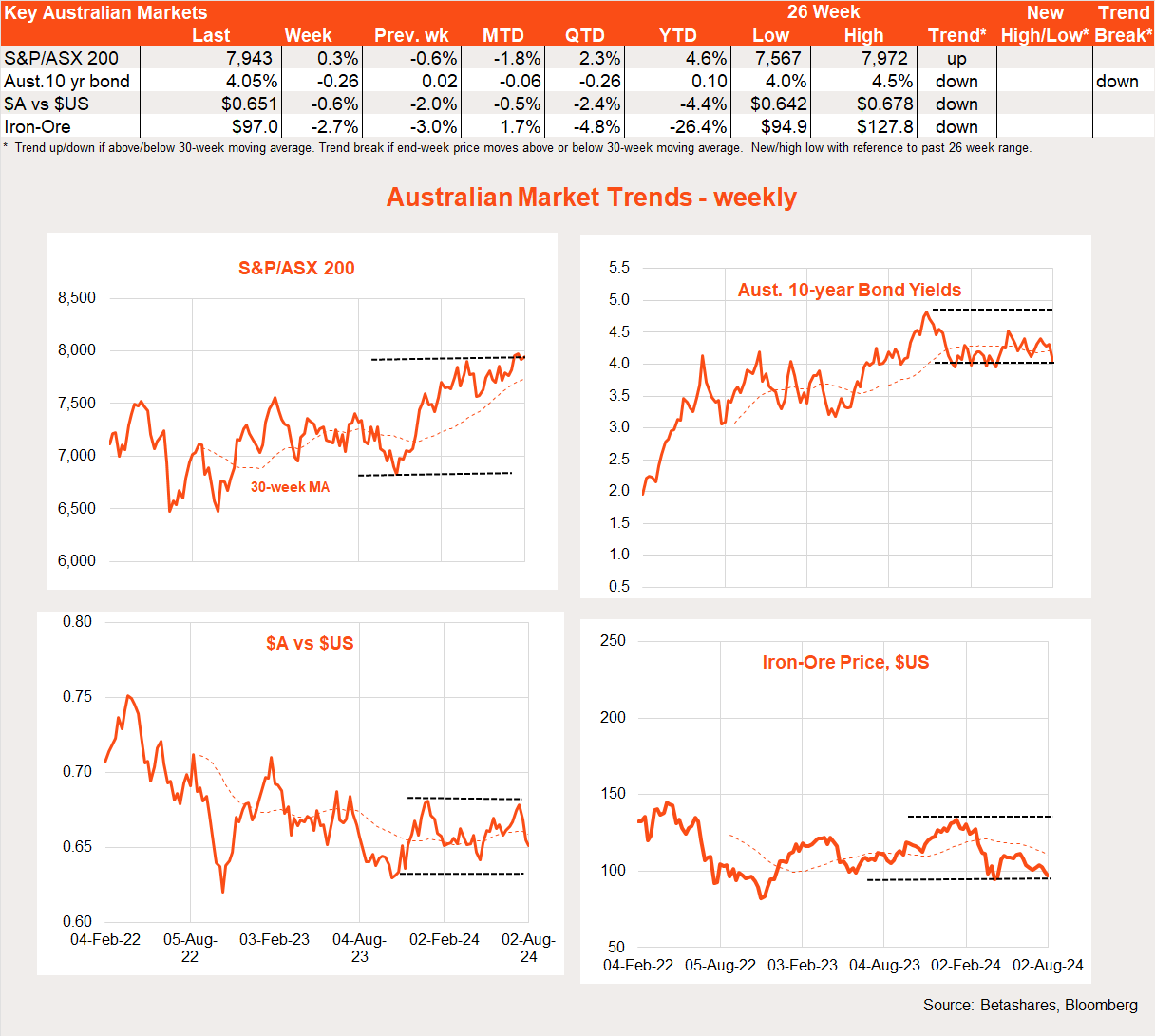

Local stocks held up last week – helped by a lower-than-feared inflation report – though are yet to reflect Wall Street’s sell-off on Friday.

The big news last week was, of course, the June quarter consumer price index (CPI) report – which came in better than feared. Annual headline inflation ticked up to 3.8% – in line with the market and the RBA’s forecast back in May. Annual trimmed mean inflation was 3.9% – a touch higher than the RBA’s 3.8% May forecast, but lower than the market’s 4.1% expectation.

All up, the inflation results were not great – but good enough to likely rule out an RBA rate hike at tomorrow’s policy meeting. New concerns over the US economy also make it less likely the RBA would have hiked even if inflation was a bit higher last week.

The local highlight this week will be tomorrow’s RBA policy meeting and quarterly Statement on Monetary Policy. With no change in rates expected, interest will focus on the Bank’s inflation forecasts and any softening in its mild-tightening bias (neither of which I expect will change much).

Have a great week!

Explore

Bassanese Bites

1 comment on this

Let us all see how close “Your Take” actually is.