India: The market's hidden giant

Thong Nguyen

6 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

As we highlighted in Part 1 of our 3-part series, momentum investing is grounded in academic research and has shown to achieve the highest of all risk premiums among established factors of value, market beta, size and quality.

However, momentum investing can be time consuming, difficult to effectively implement due to the market impact costs from higher portfolio turnover, and is susceptible to human biases.

The MTUM Australian Momentum ETF seeks to track an index that was specifically designed as a systematic approach to momentum investing that addresses some of the shortcomings traditionally associated with momentum investing.

Considerations when implementing a momentum strategy

Momentum is a trend-following strategy, hence relevant trading principles, when applied systematically, can result in more efficient outcomes. There are several trading principles that a successful momentum strategy should adopt, including:

- Removing all human biases

- Not going ‘all in’ on a single point-in-time signal

- Adding to winning positions only rather than those going against you

- Cutting significant ‘losers’ quickly

- Taking profits or trimming positions as they go deeply in favour, reducing the impact from sharp reversals

- Diversification, and

- Applying sensible position sizing

How does MTUM differ from other momentum strategies?

Typically, what occurs with a standard momentum index is that following each selection date (generally six months apart) the entire index will rebalance fully into the highest ranked momentum stocks (e.g. 50 out of 200). However, this approach goes against some of the general principles outlined above.

On the other hand, MTUM’s Index positions the portfolio at each rebalance into companies which exhibit the highest momentum scores at each of the four prior selection dates (which occur every two months). At each rebalance, the oldest selection date result rolls off and the newest selection date result is incorporated.

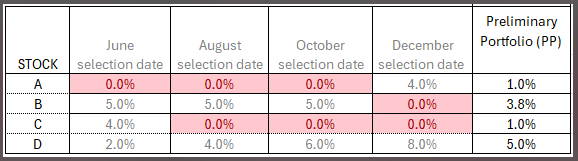

A simple illustration is provided below, showing the inclusion and weighting of 4 example stocks within the overall index stock universe.

The preliminary portfolio (PP) is the average weight of each stock at each of the prior four selection results. That is, each stock’s PP weighting is the sum of its weightings at the preceding four selection dates, divided by 4. For example, stock A has recently shown strong momentum and is assigned a 4% weight at the most recent selection date. But since it did not perform strongly enough to qualify for the portfolio at the previous three selection dates, stock A is only weighted partially at 1% (the average weight of the four prior results).

If stock A continues to outperform at the next selection date in 2-months’ time, when the oldest selection date (June in the table above) result drops off and the newest is added (February of the following year), it gets upweighted further i.e. the index only adds to positions which continue to perform well (Rule 3).

This unique positioning framework achieves the following:

- Stock positions are increased as stocks show consistent performance, with a full weight allocation built up if a stock has passed the momentum rankings at the four most recent selection dates (e.g. stock D).

- Stock D is also an example of trimming back positions vulnerable to a sharp reversal (Rule 5). As the stock continues to perform strongly, its weight in the broader market cap benchmark increases and the assigned weight at each successive selection date gets larger and larger. However, by taking the average weight over the previous selection dates, Stock D has a 5% weighting in the PP, which is lower than the December selection date alone, being 8%.

- False signals are mitigated by entering positions partially or not going all in (Rule 2). Should a stock not rank favourably in the following selection dates (implying relative under-performance), the negative contribution will be significantly reduced due to the initial partial weight entry (e.g. stock C).

- Turnover and hence market impact costs at each rebalance are significantly mitigated by partially entering (e.g. stock A) and exiting (e.g. stock B) positions rather than completely.

- Factor decay is mitigated by rebalancing the portfolio every two months (versus the typical six months) which helps keep the momentum signal fresh and identify stocks earlier which may lead to the next rally in momentum.

- Given the index holds a mix of partial and full positions, stock diversification is increased, with MTUM holding circa 90 stocks on average (Rule 6).

- Once the PP is constructed, the Final Portfolio at each rebalance incorporates fast exit rules, cutting those stocks which are in the bottom decile of performance immediately (Rule 4) along with maximum stock limits to manage single stock risk and liquidity (Rule 7).

See here for further details on the index methodology.

How has MTUM’s index performed?

Source: Bloomberg. MTUM Index refers to the Solactive Australia Momentum Select Index. Chart shows MTUM’s index performance net of MTUM’s management fees and costs of 0.35% p.a. MTUM’s inception date was 22 July 2024. You cannot invest directly in an index. Past performance is not indicative of future performance of MTUM’s index or MTUM.

Since index inception in May 2011, MTUM’s Index (net of fees) has delivered a return of 11.04% p.a., which is 2.39% p.a. above the S&P/ASX 200 Index, with a similar volatility and maximum drawdown profile, as well as a 31% increase in risk adjusted returns net of fees as measured by the Sharpe Ratio.

Source: Bloomberg. MTUM Index refers to the Solactive Australia Momentum Select Index. Table shows MTUM’s index performance net of MTUM’s management fees and costs of 0.35% p.a. MTUM’s inception date was 22 July 2024. You cannot invest directly in an index. Past performance is not indicative of future performance of MTUM’s index or MTUM.

Conclusion

MTUM provides investors the advantage of accessing a well-established and proven investment style, professionally managed and rebalanced in a systematic process. It removes major hurdles for investors looking to adopt a trend-following strategy themselves, which can be costly and difficult to implement, time consuming and distorted by human biases.

For more information on MTUM, please visit the fund information page here.

There are risks associated with an investment in MTUM, including market risk, index methodology risk, portfolio turnover risk and concentration risk. Investment value can go up and down. An investment in the Fund should only be made after considering your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available on this website.

Explore

Markets