Southern route

David Bassanese

6 minutes reading time

- Global shares

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

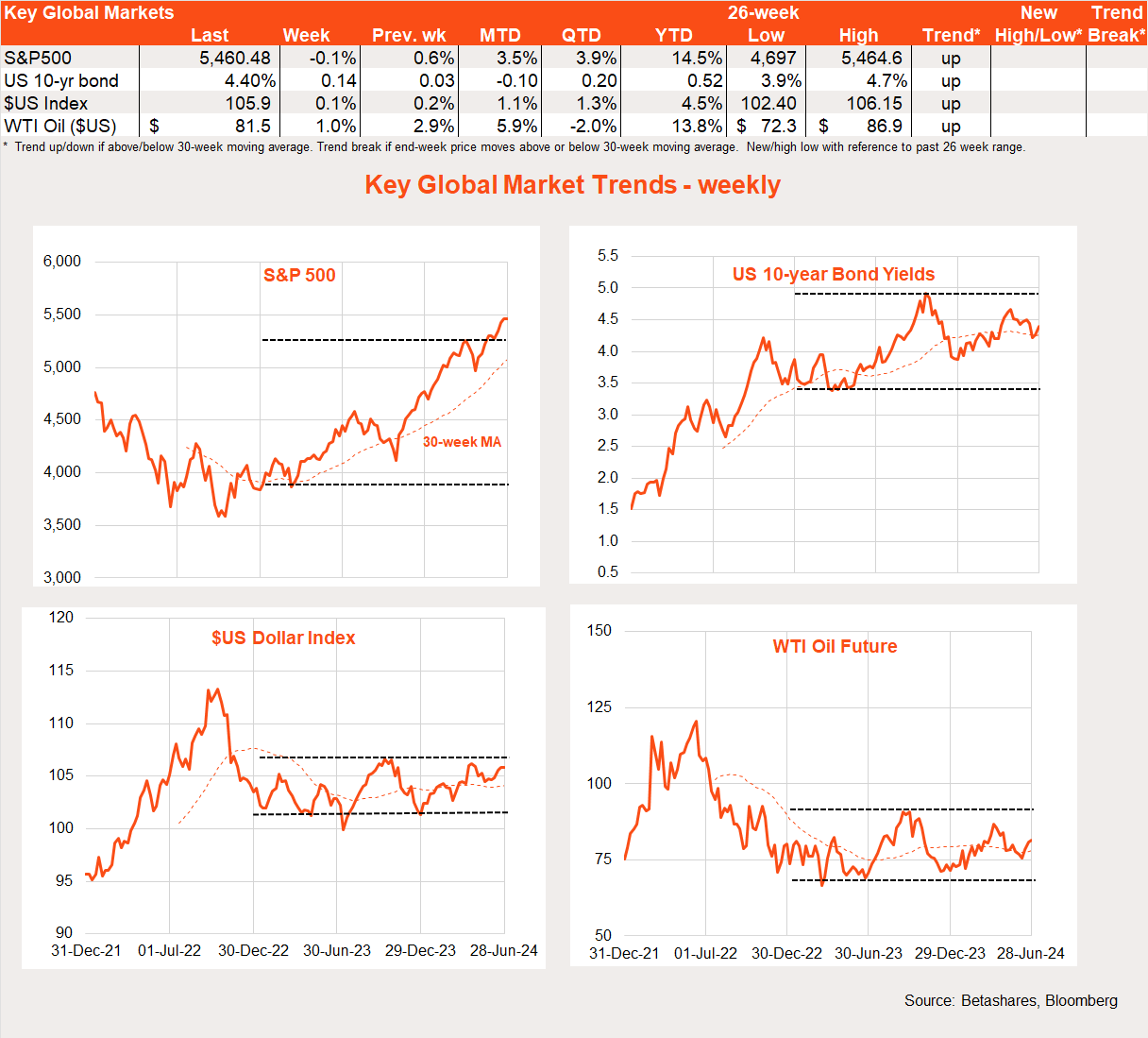

Global markets – week in review

US stocks edged back last week despite a reassuringly benign US inflation report. Buyer exhaustion and concern over the impending French elections likely held back stocks. Overall global stocks edged higher, helped by solid gains in Japan.

The major global highlight last week was Friday’s May US private consumption expenditure (PCE) deflator – the Fed’s preferred inflation measure. The core measure rose 0.1%, in line with market expectations, which allowed annual inflation to ease to 2.6% from 2.8%.

Most notable was that US stocks failed to rally on the result, suggesting the goods news was already well anticipated given benign CPI and PPI May results earlier this month.

Concern over the outcome of the French election at the weekend – with the Far Right poised to do very well – also likely held back investor enthusiasm.

As of Monday morning, the result seems to confirm the worst market fears of a resoundingly large swag of votes to the far right National Rally Party. This sets up the risk of Le Pen’s party securing an outright majority and the Prime Ministership in the second round of voting next Sunday – which would see a return to power sharing ‘cohabitation’ between the diametrically opposed Far Right and centrist President Emmanuel Macron.

Of most concern to markets is what a National Rally hold on power would mean for the stability of the European Union, the war in Ukraine and French fiscal policy. As former UK Prime Minister Liz Truss found out, markets may not take too kindly to big spending promises in the face an an already large budget deficit. The French result could also help boost the prospect of Far Right victories in other European countries.

All up, European financial markets are likely to face increased risk over coming weeks, thwarting hopes for a rotation away from the more expensive US market. As evident last week, Japan may be one beneficiary of the flight from Europe.

Whilst on the subject of politics, the resounding victory of Trump in last week’s US Presidential debate did not appear to affect markets all that much – suggesting Wall Street seems reasonably comfortable with his possible return to power. Of note now is whether Biden continues in the campaign or Democrats seek to parachute in a new candidate at the 11th hour.

Also of some note last week – given the upside inflation surprise in Australia – Canada’s May CPI result was higher-than-expected, suggesting the inflation dragon has yet to be completely slain globally.

The week ahead

The week begins with markets likely digesting results from the first round of the French election. Fed chair Powell and ECB President Lagarde are scheduled to comment on monetary policy at a forum on Tuesday. We also await the Eurozone CPI and minutes to the last Fed meeting on Tuesday and Wednesday (US time) respectively. The former will help determine how quickly the ECB cuts interest rates again.

US job openings on Tuesday will also be keenly watched, with a further decline (from still high levels) expected, which would support the view of easing labour market imbalances.

The week’s highlight will be Friday’s US June payrolls report, with another solid jobs gain of around 190k expected. Markets will be hoping for a further moderation in average hourly earnings, with a 0.3% monthly gain expected (compared to 0.4% in May).

There have been tentative signs of an easing in both US consumer spending and labour demand so far this year – which, at this stage, markets still regard as a welcome sign of a ‘soft landing’ and lower interest rates ahead. We’re not there yet, but one risk is a possible inflection point in coming months where markets come to fear rather than welcome slowing US economic growth.

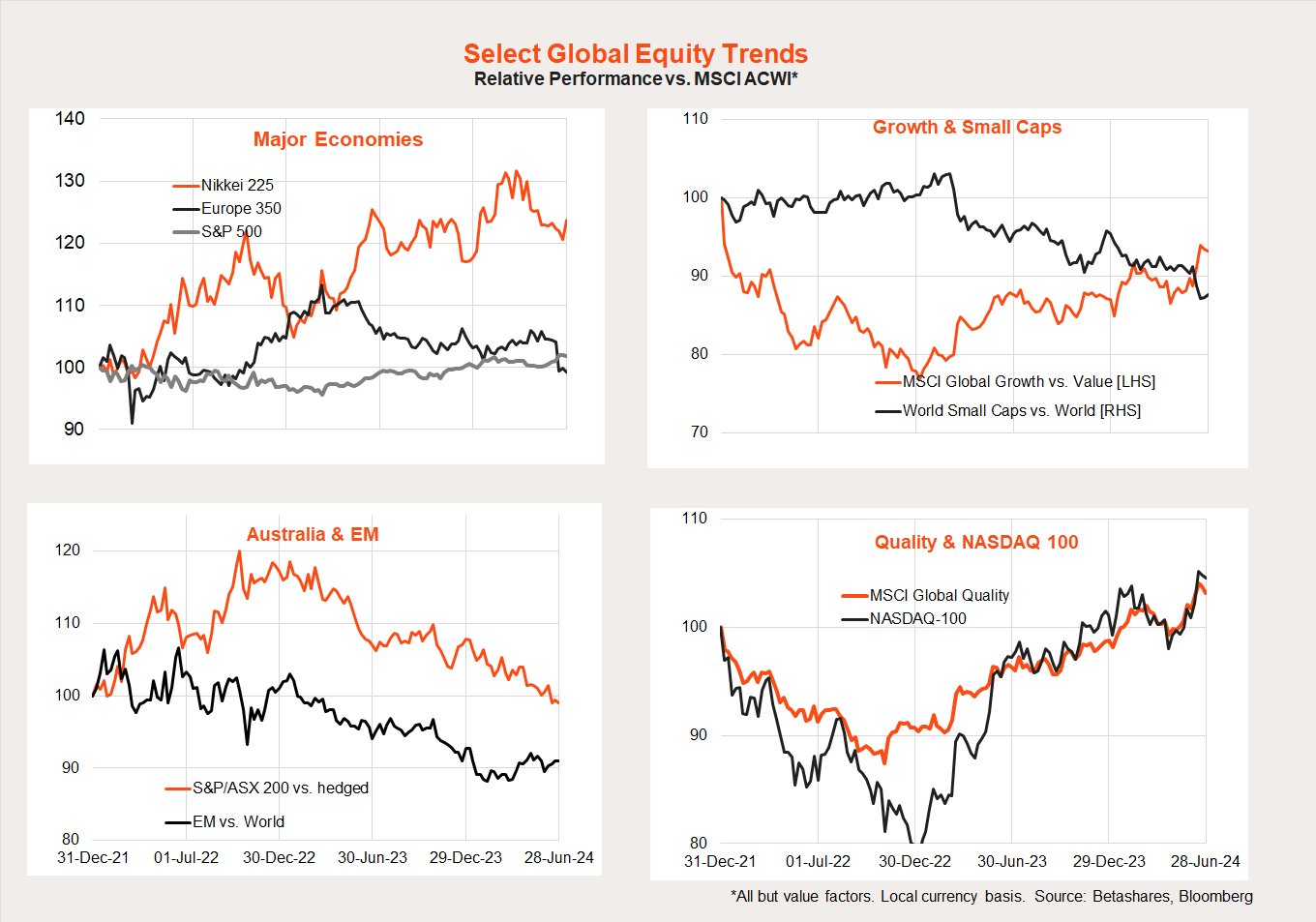

Global equity trends

Concerns around the French election have seen relative European equity performance slump of late, with (as noted above) one potential beneficiary being Japan.

There was also a modest correction in growth relative to value last week, with the latter helped by strength in energy stocks.

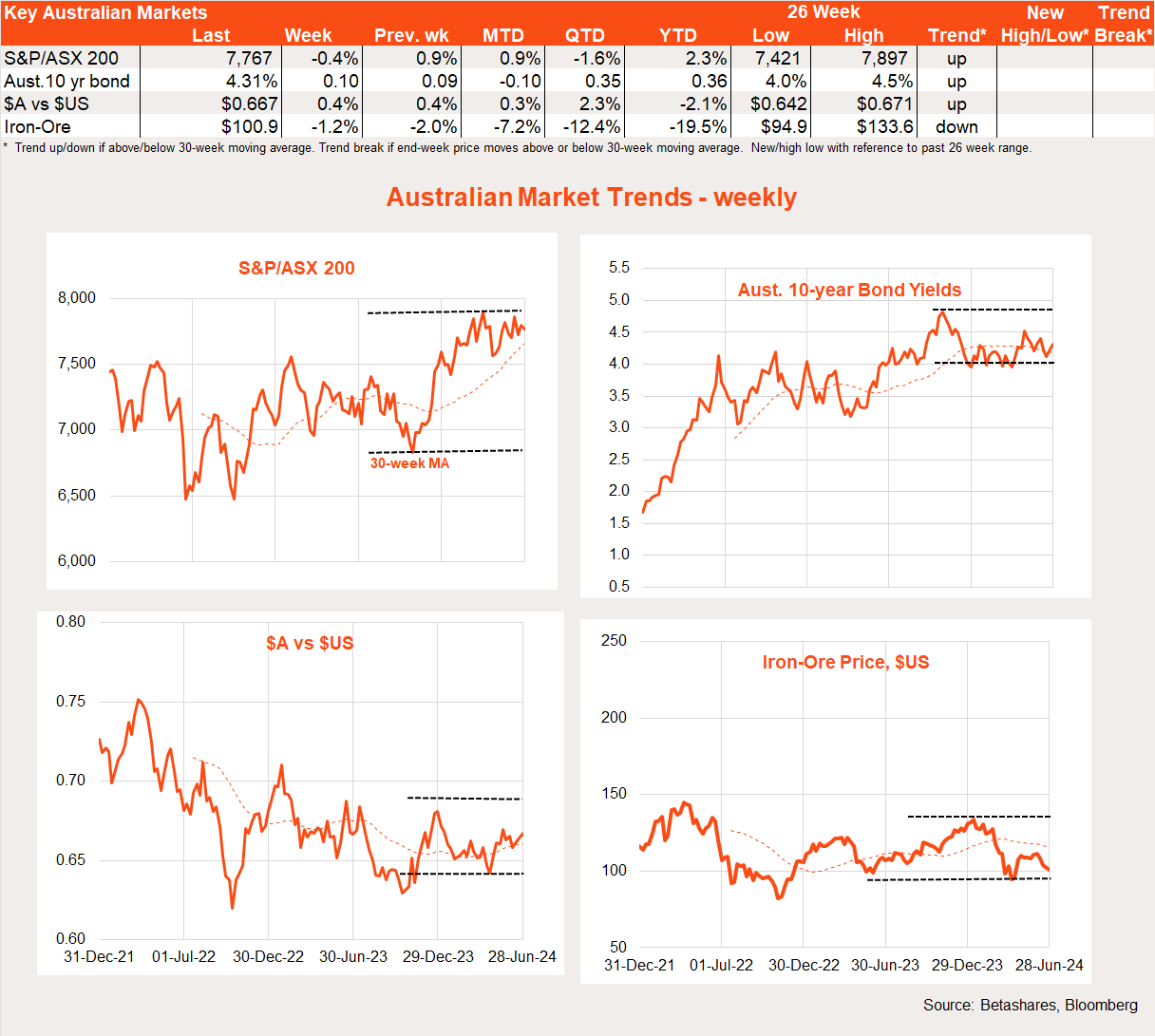

Australian markets

The S&P/ASX 200 eased back 0.4% last week, not helped by a higher than expected May CPI result and heightened talk of a potential RBA rate hike in August.

Last week I alluded to the increased risk of an August rate hike given hawkish comments from RBA Governor Bullock the previous week. In particular there appeared the risk of a hike if the June quarter CPI on July 31 came out higher than expected (i.e. more than, say, 0.8% quarterly gain).

One week later, the May monthly CPI was higher than expected – heightening the risks around the June quarter result.

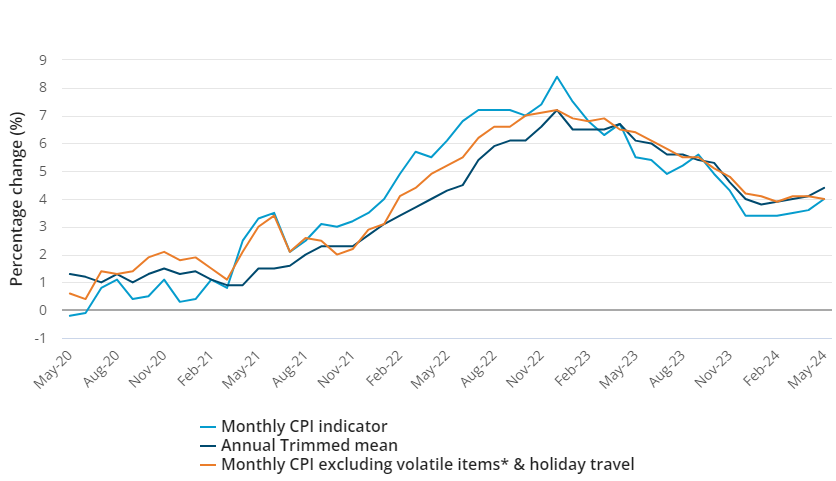

While the monthly CPI reports contain partial information and tend to be volatile, stepping back from the month-to-month noise, one clear disappointing signal emerged – annual inflation across various measures has failed to decline much further in 2024, and remains stuck at an uncomfortably high level of around 4%.

Most concerning, annual trimmed mean inflation jumped from 4.1% in April to 4.4% in May. The seasonally adjusted annual inflation rate jumped from 3.8% to 4.1%. Excluding volatile items and holiday travel, annual inflation did ease modestly from 4.1% to 4.0% – but remains too high.

Monthly CPI Measures (YoY%)

Source: ABS

It is still not a done deal that the RBA will raise rates in August. I still think the quarterly increase could hold to 0.8% or less (which would be consistent with the RBA’s latest forecasts of 3.8% annual inflation for both the headline and trimmed mean) allowing the RBA to likely stay put. Another ‘out’ would be if activity data in coming weeks softened abruptly – which I don’t expect.

All up, I still attach around a 40% chance to a rate hike in August – but I’m a little more nervous than I was before the May CPI result.

Turning to the week ahead, house prices are out today, minutes from the previous RBA meeting on Tuesday and retail sales and building approvals on Wednesday. There’s a risk the minutes confirm the RBA’s apparent more hawkish shift in recent weeks. Otherwise, data should be mixed, with still firm house prices in June, yet soft retail spending and home building approvals.

Have a great week!

Explore

Bassanese Bites

1 comment on this

Ha, Ha, sounds like you are doing the economist shuffle, right, left, up, down.

Interesting times are ahead, a serious adjustment is near.

Meanwhile Gold, Silver is waiting in the shadows.

Meanwhile, I am told, that United Global Capital in Melbourne appears to have closed its doors.

stay safe and warm