Same hedge, different tax outcome: one key consideration when comparing global bond ETFs

David Bassanese

5 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Global markets

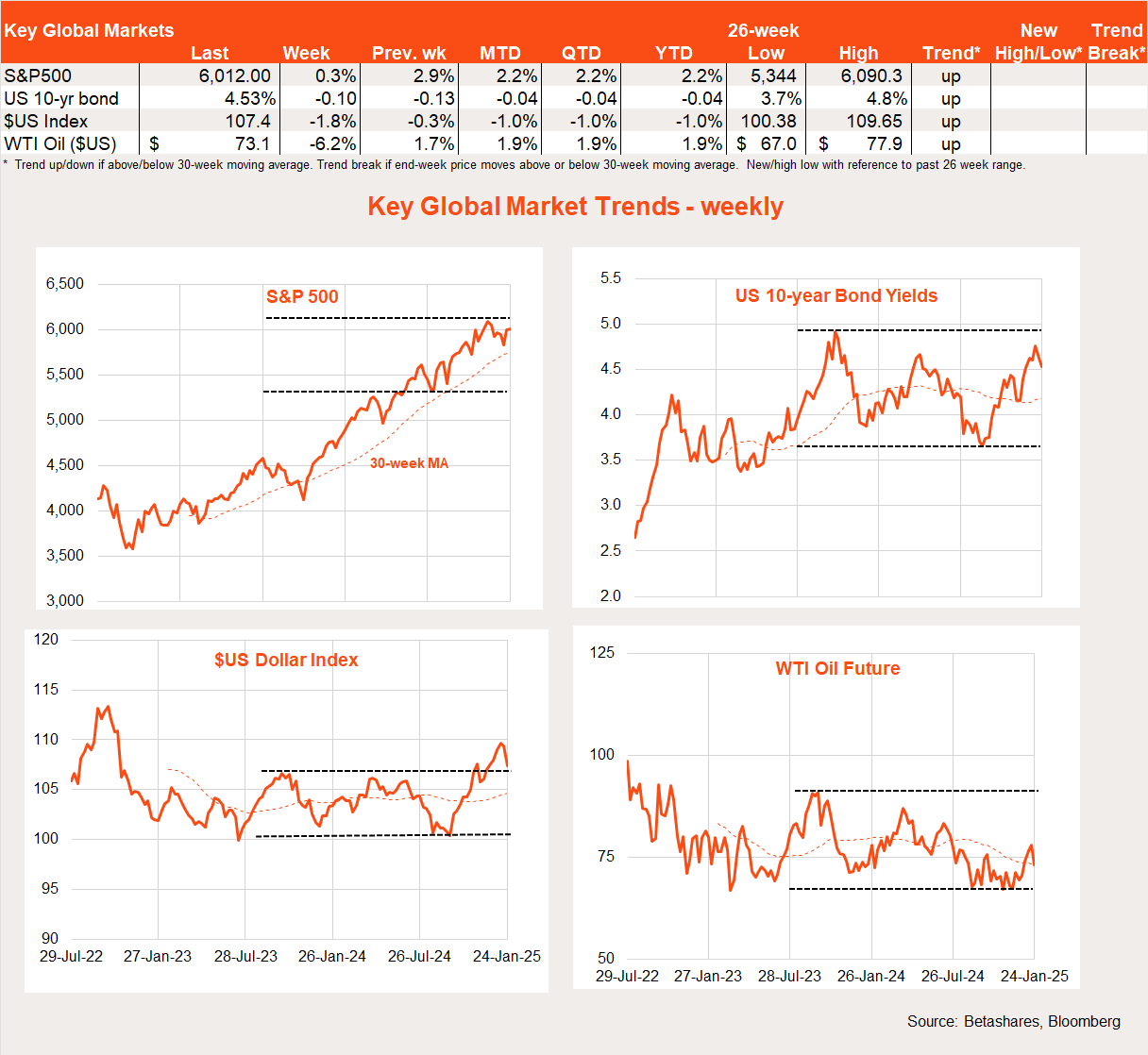

Updated for last night’s close, US stocks were up modestly over the past week helped by relief on the trade-war front. However, US stocks fell on Friday and more so overnight due to a major new threat to the prevailing AI narrative.

2025 has started with a bang. First the good news: markets enjoyed early relief last week with US President Trump refraining from imposing new tariffs on major trading partners in his first days in office. That said, he’s still swinging the tariff stick on a daily basis, leaving markets guessing.

The bad news (at least for those stocks enjoying the current AI narrative) was the release of incredibly impressive results from China’s AI start-up DeepSeek, which has quickly become a deep concern to Silicon Valley. In short, DeepSeek claims it can deliver similar AI performance to ChatGPT and Gemini with less expensive chips and less power use – what’s more, it’s free!

If so, the premium attached to Nvidia’s best chips is immediately in question, as is the ability of Alphabet and Microsoft to monetise their AI offerings, not to mention the reduced value of energy companies as the likely power demands of AI are re-assessed. Talk about tech disruption!

Of course, what is bad news for existing AI producers potentially is good news for budding AI users and application developers – in much the same way, perhaps, as the skills associated with building and maintaining websites in the late 1990s tech boom were quickly commoditised. Although the premium attached to the value of many early internet companies quickly evaporated, it did not stop the ongoing internet boom and ensuing digital revolution. As with the internet, ever-cheaper AI technology is also deflationary.

From an immediate market perspective, however, the problem is many of the current winners of the AI boom appear at most risk of disruption, and most of the future winners either aren’t yet listed or are still too hard to identify (although Meta, Apple and Salesforce, as major AI users, have so far seen market gains). In any case, the continued outperformance of the technology sector, and even the US market, is clearly in question.

Provided the macroeconomic backdrop remains good, however, it need not spell the end of the equity bull market but rather a rotation both within technology and towards non-technology. If this really is the end of US exceptionalism and cheaper technology it could also help drag down the US dollar and bond yields.

In other global news last week, the Bank of Japan raised rates, as widely expected – though unlike the surprise move in August last year, it barely caused a ripple in markets.

Global week ahead

While markets are likely to continue to mull the implications of the DeepSeek shockwave this week, there’s also a host of other key events.

For starters, the Fed meets on Thursday and Friday (US time). While no rate cut is expected, markets will focus keenly on the hawkishness of Fed rhetoric and what it means for the probability of a rate cut in March.

Friday also sees the release of important price and wage data. The Fed’s preferred inflation measure is released for December, with annual growth in core consumer prices expected to hold steady at 2.8%. Annual growth in the employment cost index is expected to remain firm, although ease in Q4 from 3.9% to 3.8%.

Last but not least, US Q4 GDP is released on Thursday, with healthy 2.7% annualised growth expected.

Barring surprises, these growth and inflation results will play into the idea that the Fed is in no hurry to cut rates again any time soon.

Global market trends

It’s early days, but the DeepSeek shockwave poses a major new threat to the US/technology outperformance trend of recent years – more updated relative performance charts will be provided next week as the dust settles on last week’s volatility.

Australian market

Based on early morning trading, the S&P/ASX 200 is up 1% over the past week and has held up relatively well so far this morning. This is consistent with the idea that the DeepSeek shock could favour global equity market rotation, rather than weaker markets overall.

There was little local data of note last week. The focus this week will be on tomorrow’s Q4 CPI report. As it stands, the market expects annual trimmed mean inflation to ease from 3.5% to 3.3%, which would be just under the RBA’s November forecast of 3.4%.

Is that enough to secure a rate cut next month? To my mind, 3.3% would be good but still leave next month’s rates decision line-ball – interestingly only 40% of economists surveyed last Friday expected a February rate cut, though the market attached an 80% chance.

Based on the low November CPI result and the easing in house prices over Q4, I now expected the trimmed mean annual rate to drop to 3.2%, compared to my earlier forecast of 3.4%. This is a more notable downside surprise to the RBA’s forecast and, if right, I’d then expect the RBA to cut rates next month.

Have a great week!

1 comment on this

G’day David,

Thanks for the Bite.

Just wondering if you could expand on and share your thoughts on the below statement;

“In other global news last week, the Bank of Japan raised rates, as widely expected – though unlike the surprise move in August last year, it barely caused a ripple in markets.”

The reason I ask is because that carry trade shock last year was quite big so I was surprised there was no reaction this time round despite the move being widely expected as you note.

Thank you.