All in on AI? 3 ways to reduce concentration risk

David Bassanese

5 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

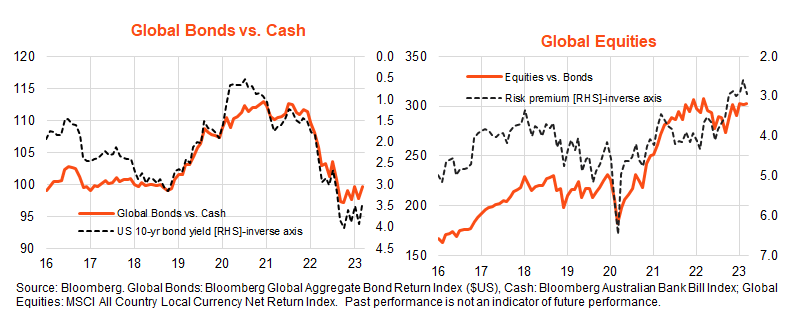

Global equities and bonds

Global equities bounced back in March as February’s fears of persistent inflation and aggressive central bank interest rate increases (i.e. a ‘no landing’ scenario) were eased by a period of global banking instability.

Markets ended the month hoping a degree of self-imposed credit tightening by US banks will help slow US economic growth without the need for further aggressive interest rate increases by the Federal Reserve. Still high, but lower than expected US inflation reports – along with still firm economic activity – also boosted US ‘soft landing’ hopes.

In hedged terms, global equities rebounded by 2.4%, after a decline of 1.9% in February. Further weakness in the $A saw a stronger 3.8% gain in global equities on an $A or unhedged basis over the month.

Reduced central bank tightening fears also boosted bond returns, with the Bloomberg Global Aggregate Bond Index returning 2.1% in $A hedged terms after a 1.8% decline in February.

As seen in the chart set below, global bonds have made modest gains over cash with the easing in bond yields since their month-end peak in October. Supported by a narrowing equity risk premium, global equities have also generally outperformed global bonds since end-September despite weak earnings growth over this period.

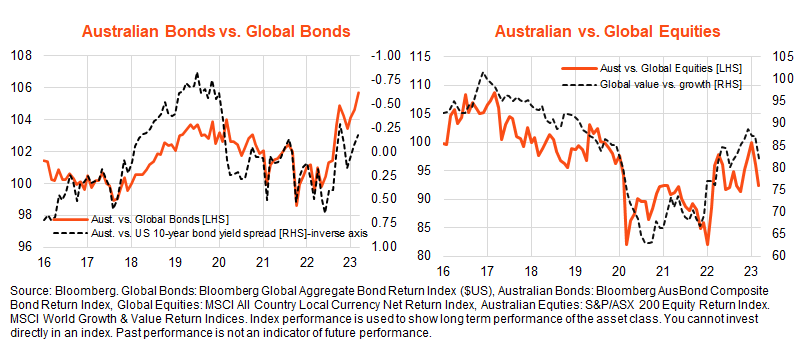

Australia equities and bonds

Australian bonds outperformed global bonds again last month, helped by a narrowing in interest-rate differentials as the Reserve Bank provided stronger signals regarding a potential pause in rate hikes. A slowing in consumer spending and an easing in monthly inflation reports have helped in this regard. The Bloomberg Australian Composite Bond Index returned 3.2% in March after a 1.3% decline in February.

Australian equities, by contrast, underperformed, with the S&P/ASX 200 down 0.2% in March. This is consistent with recent global banking instability weighing on financial relative to technology stocks, which has weighed on the value relative to growth equity factors.

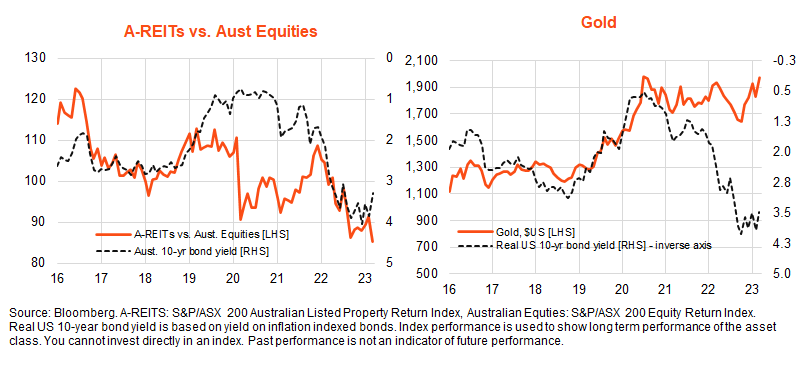

Listed property and gold: benefiting from ‘soft landing’ hopes

Despite an easing in bond yields, the Australian listed-property sector suffered a significant 6.8% fall in March, likely reflecting concerns that a tightening in global lending conditions would hurt valuations. Last month’s slump in property returns has unwound the tentative signs of relative performance improvement against Australian equities since the peaking in bond yields late last year.

Gold, by contrast, benefited from the easing in bond yields and a softer $US, with the price in $US terms up 7.8% in March. Gold has continued to broadly benefit since late last year from US soft landing hopes.

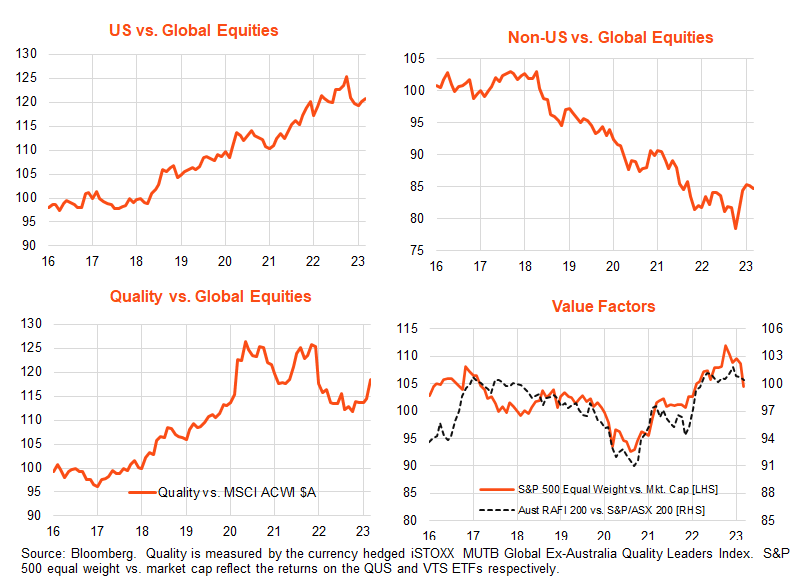

Equity factors: value, growth and quality

Soft landing hopes and recent global financial instability boosted returns from the growth/technology sectors compared to the financial/value sectors last month, which in turn saw US equities outperform non-US equities.

The rebound in US performance followed several months of underperformance – despite the relative outperformance of growth over value. In turn, this reflected a solid bounce back in European equities, as fears of an energy-induced recession abated.

Global quality continued to outperform in March, a trend that has now been in place since the peaking in bond yields late last year. By contrast, the pull-back in relative performance by value exposures such as the S&P 500 equally weighted index (QUS ETF) and the fundamentally weighted Australian equity ETF (QOZ) has continued.

Outlook

Whether or not the US economy can pull off a soft landing remains the critical driver of global market trends. Prior to the recent increase in global banking instability, renewed fears of an overly strong US economy were beginning to outweigh hopes of a soft landing that had been in place since around October last year.

We’re now in a state of flux. If global banking concerns ease, earlier fears of strong US growth and inflation could easily re-emerge. While there has been an encouraging easing back in US price inflation over the past month, it still remains too high, as does wage growth in a still-tight labour market.

My base case still errs towards stubbornly high US wage and price inflation and so an eventual US recession – caused by a tightening in lending conditions and/or aggressive further Fed rate hikes. Indeed, history suggests it will be hard to get US inflation sustainably lower without a material weakening in the still very tight labour market.

The resilience of the US economy and the degree of monetary tightening required to get this hard landing, however, will determine whether we need to go through a ‘no landing’ scenario again before we get there.

Further information on the complete range of Betashares exchange traded products can be found here.

Explore

Markets